Download PowerPoint versions of both figures.

Navigation

-

Lenses

This content is ...

Affiliated with (What does "Affiliated with" mean?)

-

Recently Viewed

- This feature requires Javascript to be enabled.

Inside Collection (Book): American Health Economy Illustrated

12.4 Per Capita Health Spending Increases with Age

Summary: Per capita health spending generally increases with age; annual health costs for the elderly are at least four times as high as for children and young adults.

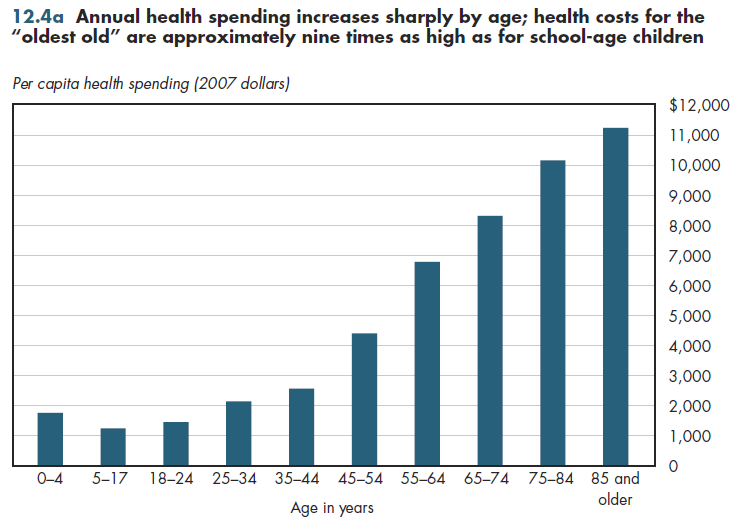

Total health spending by the "oldest old" is approximately nine times as much as is spending by school-age children (figure 12.4a). These numbers are for only the civilian non-institutionalized population. Because approximately one in six of the "oldest old" (age 85 and over) are in nursing homes and the average annual cost of a nursing home stay exceeds $75,000, this ratio would be considerably higher were costs of the nursing home population included.

The relatively low expense for children helps explain why it has been easier politically to secure expansions in Medicaid and SCHIP coverage for children rather than for non-elderly adults. Expenditures at childbirth are one important reason why pre-school health spending is higher than for school-age children. Forty percent of births are covered by Medicaid, which contributes to higher spending in the postnatal period, especially for newborns who otherwise would have been uninsured.

Conversely, the relatively low spending among those ages 18-34 helps explain why these so-called "young invincibles" tend to have a much higher rate of being uninsured. In the group market, premiums are community-rated, which often makes them not a particularly good deal for young adults unless the employer substantially subsidizes the premium. In some states, the non-group market also faces community- rating restrictions or what is called "modified community rating." In many of these states, insurers can offer different rates based on age but within rating bands. The new health reform law will do the same. The difference between premiums for the most expensive age category and the lowest ages cannot vary by more than a factor of 3:1, even though it is clear from figure 12.4a that actuarially, the cost difference between age categories is substantially greater. The consequence will be higher rates for young adults than they would otherwise face in a less regulated environment.

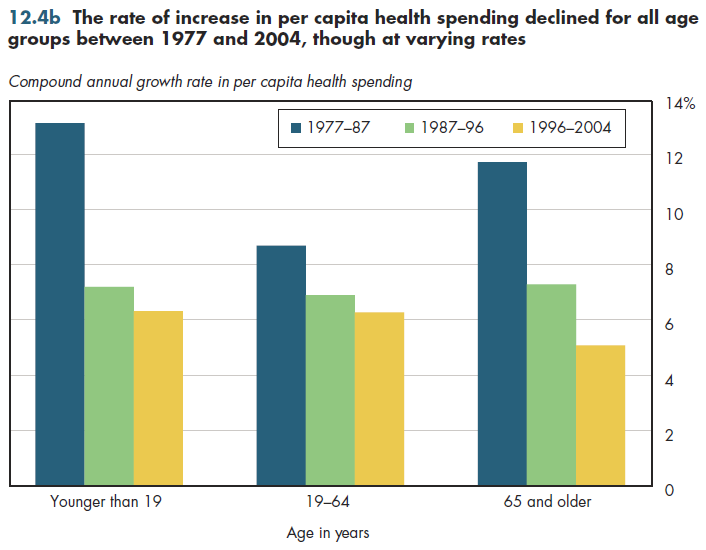

Between 1977 and 2004, the average annual increase in expenditures declined for every major age category (figure 12.4b). These declines were much greater for children and the elderly than for other groups. Should the health reform law be fully implemented, this downward trend might reverse itself for two reasons. First, the expansion of coverage to tens of millions of uninsured will boost their previous levels of spending. Second, various regulations are having the effect of increasing premiums in the short run.

Downloads

References

- Department of Health and Human Services. Agency for Healthcare Research and Quality.

- Department of Health and Human Services. Centers for Medicare and Medicaid Services.

- Waldo DR, ST Sonnefeld, DR McCusick and RH Arnett III. Health Expenditures by Age Group, 1977 and 1987. Health Care Financing Review 1989; 10(4):111-20.

Collection Navigation

- « Previous module in collection 12.3 Burden of Paying for Health Care Has Increased

- Collection home: American Health Economy Illustrated

- Next module in collection » 12.5 Difference between Men and Women's Health Costs Depends on Age

Content actions

Give feedback:

Download:

Add:

Reuse / Edit:

Footer

More about this module: Metadata | Downloads | Version History

This work is licensed by Christopher Conover under a Attribution (CC-BY 3.0), and is an Open Educational Resource.

Last edited by Jia Yao on Sep 26, 2013 1:48 pm -0500.

Twin Cities Campus:

- © 2012 Regents of the University of Minnesota. All rights reserved.

- The University of Minnesota is an equal opportunity educator and employer. Privacy

- Last modified on Sep 26, 2013 1:48 pm -0500